Credit Weekly: The Dip That Doesn't Fade

The playbook requires three conditions. All three are broken.

🚨 Connect: Twitter | Instagram | Job Board

You’ve seen this before.

Geopolitical shock, spreads widen, everyone holds their position and waits. It worked after Ukraine. It worked after every Middle East flareup in recent memory. The institutional muscle memory is so deep that most investors aren’t even making a conscious decision anymore.

They’re just holding. Assuming the premium fades because it always has.

Maybe it does this time too.

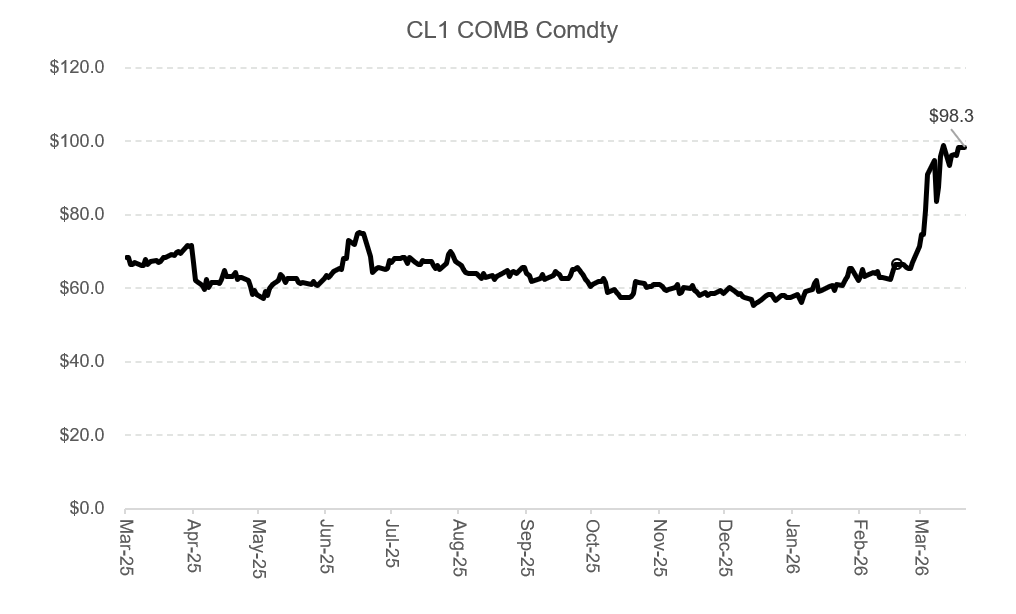

But the mechanism that allowed the market to look past prior conflicts was a specific one: the underlying economic damage was containable enough that pricing it out felt rational within weeks. Prior conflicts didn’t close a chokepoint carrying nearly 20% of global oil supply. They didn’t leave years-long damage at one of the world’s most important LNG export hubs.

The geopolitical risk premium faded because the physical reality underneath it eventually stabilized.

That’s the assumption that’s harder to make here. And it’s the one current spread levels are still relying on.

The Three Conditions

The geopolitical dip trade works when three things are true simultaneously.

Central banks can ride to the rescue. Shock hits, growth slows, the Fed cuts, liquidity floods the system, assets recover. This is the mechanical engine behind every successful dip-buy since 1987. Shock happens, Fed responds, dip gets bought.

Investors have dry powder. Buying dips requires capital on the sidelines ready to deploy. Institutional cash is sitting at lows. The ammunition that funded every dip-buy of the past decade was systematically deployed into a market that went essentially straight up from October 2022 through January 2026.

The shock is demand-driven, not supply-driven. A demand shock hits growth and pushes inflation down. That gives the Fed room to cut. Supply shocks work the opposite way. They hit growth and push inflation up simultaneously. The Fed cannot ease its way out of stagflation. Cutting into a supply shock makes the inflation problem worse. The central bank is paralyzed precisely when the market most needs it to act.

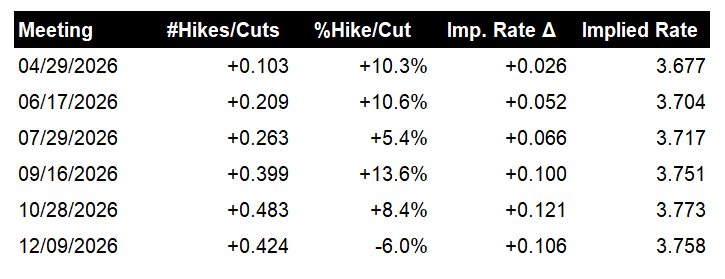

Right now all three conditions are inverted. Seven FOMC participants already see zero cuts this year. Markets are pricing a chance of a hike by year-end, a complete reversal from the 2.5 cuts priced three weeks ago. Dry powder is near multi-year lows. And Iran is a supply shock.

Rates First, Spreads Second

So if this isn’t a normal dip, what is it actually?

The easiest mistake right now is assuming credit is selling off because credit fundamentals suddenly cracked. That’s only part of the story.

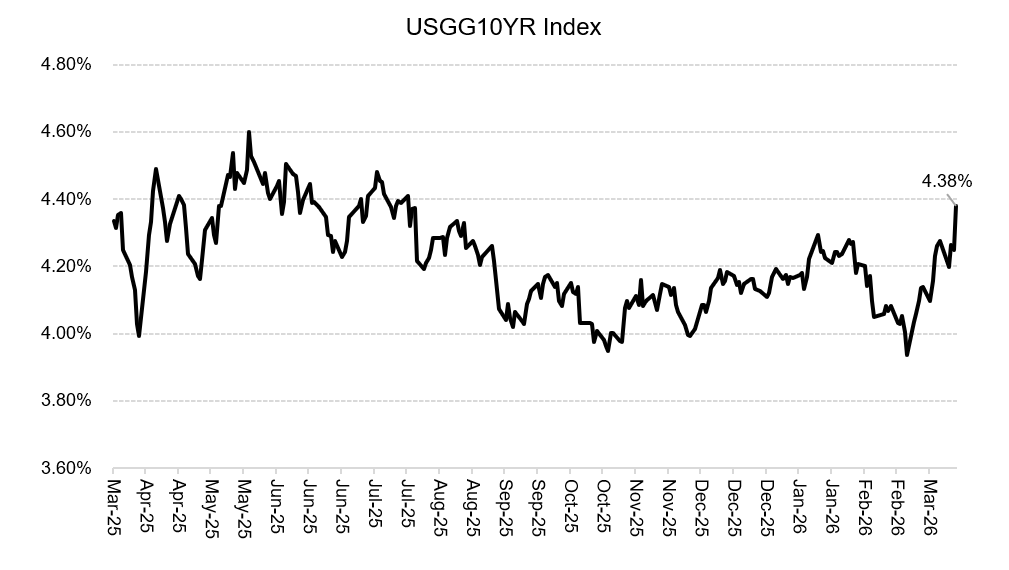

This is a rates selloff first, a spread selloff second, and a credit event only after that. Treasury yields have backed up sharply, rate-cut expectations have been pushed further out, and the market is repricing toward higher-for-longer just as Iran makes the inflation backdrop harder to dismiss.

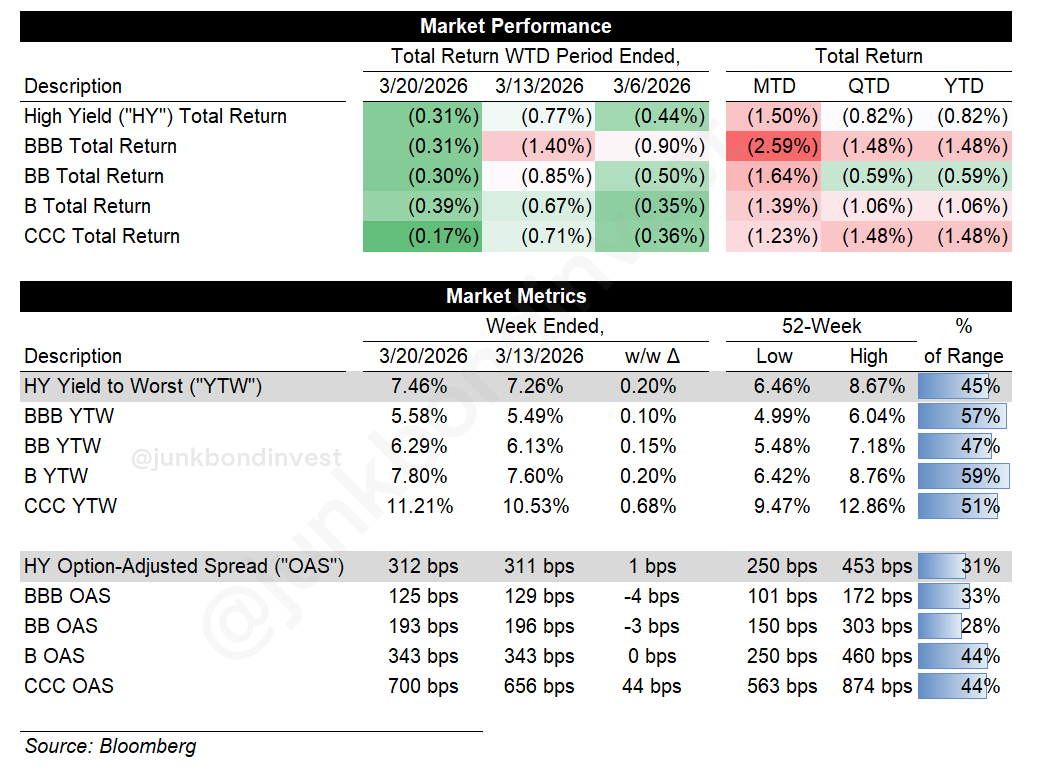

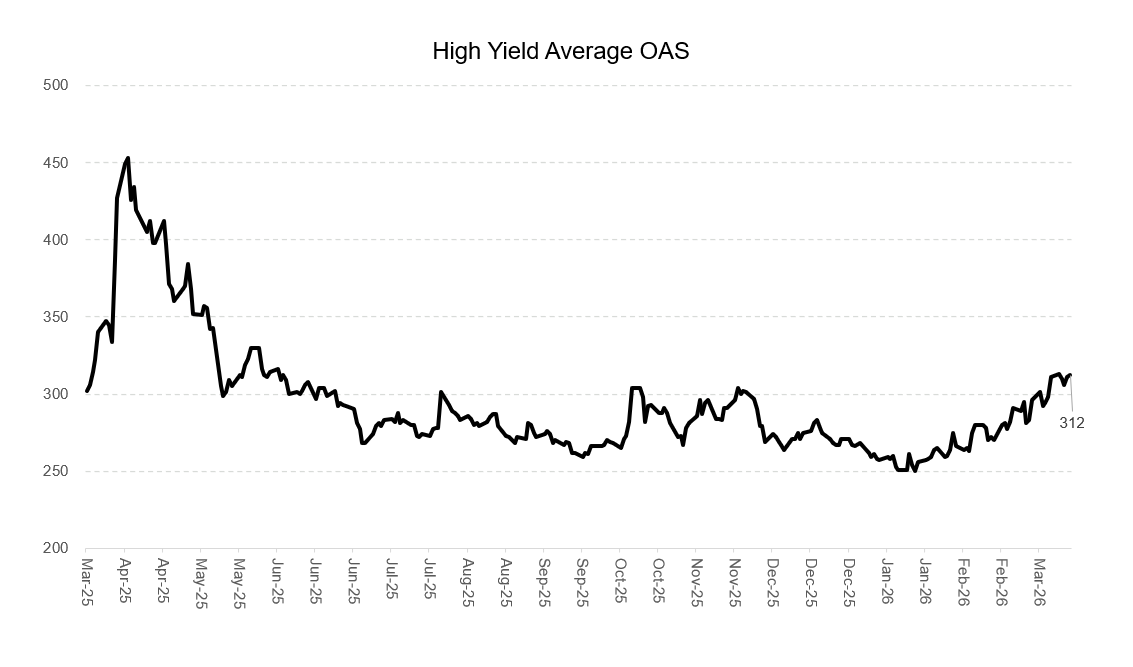

HY yields are back near nine-month wides but a meaningful part of that move is coming from the risk-free rate, not from a collapse in credit quality.

That distinction matters because it tells you what kind of selloff this actually is. If this were a classic credit panic you would expect more obvious distress in the lower-quality tail and more indiscriminate spread widening. Instead you are seeing a macro tightening event working its way through leveraged credit.

Spreads are wider but they are not anywhere near recession pricing. The market is repricing assumptions around inflation, rates, and funding conditions before it is repricing broad insolvency.

It also explains why BBs are not behaving defensively. In a normal risk-off move investors hide in quality. In a rates-driven selloff BBs give you more duration and less spread cushion. They get hit because they are not paying you enough to absorb the rate move.

But the more uncomfortable setup is one level down. Single-B credits don’t need perfection. They just need the world to stay good enough. Margins can’t weaken too much, financing windows can’t stay difficult too long, interest costs can’t remain punitive quarter after quarter.

A slow-burn shock erodes exactly those assumptions one quarter at a time without triggering the kind of visible distress that forces a repricing. The real danger may not be the credits everyone already knows are broken. It may be the ones still priced as if normal refinancing conditions are only temporarily delayed.

The Comment Worth Sitting With

Before the credit mechanics, one piece of context that matters.

Treasury Secretary Bessent said publicly last week that Kharg Island could eventually become a US asset. 90% of Iran’s oil exports transit Kharg. Whether he meant it literally or was sending a signal is almost beside the point. Once it’s said publicly, Iran’s ability to negotiate a face-saving exit narrows considerably. The incentive to sustain asymmetric disruption rather than deal increases. That’s a probability shift on conflict duration that spread levels haven’t moved to reflect.

And regardless of how the conflict resolves, some of the damage is already permanent. Qatar confirmed multi-year damage to Ras Laffan. 15 million tonnes of LNG annually offline for 3 to 5 years. A ceasefire tomorrow doesn’t rebuild that infrastructure. The damage already done locks in supply tightness for years regardless of the diplomatic calendar.

The Commodity Transmission Nobody Priced

Oil up 30% since Iran escalated doesn’t stay in the energy sector. It moves through the cost structure of every manufacturer with hydrocarbon exposure. Leveraged credit is loaded with them.

Start with autos. The auto supplier book runs on petroleum-based raw materials and energy-intensive manufacturing processes. Margin pressure that was theoretical six months ago is now arithmetic. Sponsors underwrote these businesses at commodity prices that no longer exist. Pass-through mechanisms that looked adequate in a stable environment are proving inadequate in a spike. The backend of the capital structure is repricing to reflect that.

Building products is a different problem but the same pattern. Soft housing, no policy support, PE-backed structures built for a rate environment that never materialized. The sector had a weak earnings season and private issuers haven’t fully reported yet. Price discovery isn’t done. The names already trading poorly are probably the honest ones.

Chemicals and packaging are getting compressed from both sides simultaneously. Rising resin and energy costs on the margin side, potential feedstock disruption from supply chain complications on the input side. That’s a squeeze with two blades in a sector carrying leverage that was sized for neither.

The through-line across all three is the same. Commodity shock plus leverage plus rate sensitivity plus zero margin for error. That formula was always going to find its victims. It’s finding them now.

There is also a second-order effect that hasn’t fully shown up yet. If the disruption lingers, the first real damage may not appear in earnings. It may appear in working capital.

Companies carry more inventory because they don’t trust transit times. Freight and insurance costs rise. Suppliers tighten terms. Customers pay more slowly because they’re managing the same uncertainty on their end.

EBITDA can look fine for a quarter or two while cash gets trapped in the plumbing. That’s how an operating problem becomes a credit problem. Not with one dramatic miss but with weaker cash conversion, more revolver draws, and less covenant cushion before the headline numbers tell you anything.

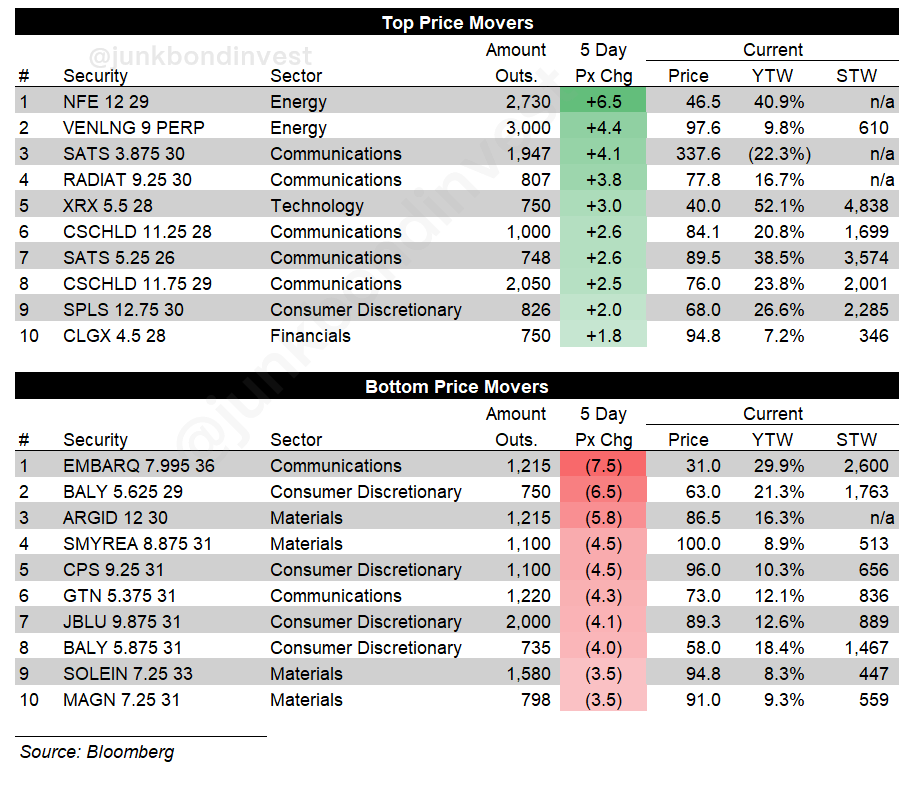

The Primary Market Is Open. That’s the Problem.

Only one HY deal priced last week. One.

This week’s pipeline is $15+ billion as larger M&A financings come forward (e.g., EA, Nexstar). That tells you capital markets are still functioning. It also tells you issuers are facing a much worse buyer base than they were a few weeks ago.

Fragile markets are often more dangerous than shut ones. A shut market is obvious. A fragile one encourages issuers to believe financing is still available right up until it isn’t. Deals can still get done. They just need more concession, more structure, and better timing.

How $15+ billion clears into a market with fresh redemption pressure and a deteriorating technical backdrop will be more informative than any spread quote this week.