Credit Weekly: The Biggest Deal Since The GFC Priced This Week

The primary market is celebrating. The secondary market is telling you something else.

🚨 Connect: Twitter | Instagram | Job Board

You were watching the order book.

Fifty billion dollars in orders. Priced at the tight end of talk. Three EA 0.00%↑ bond tranches, all trading up on the break. Every desk with a story about how oversubscribed the deal was. Oil above $100, 10-year at eight-month highs, and the market took it down without flinching. You were telling yourself this was a sign of health.

Meanwhile the secondary market was bleeding. Quietly. Right next to you. Same screen.

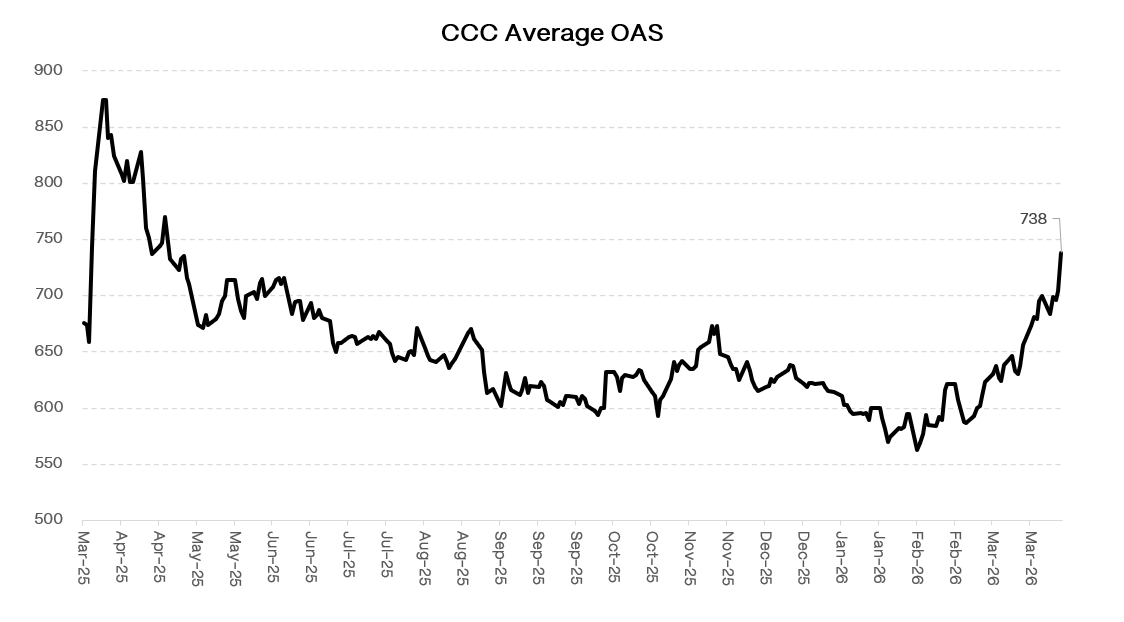

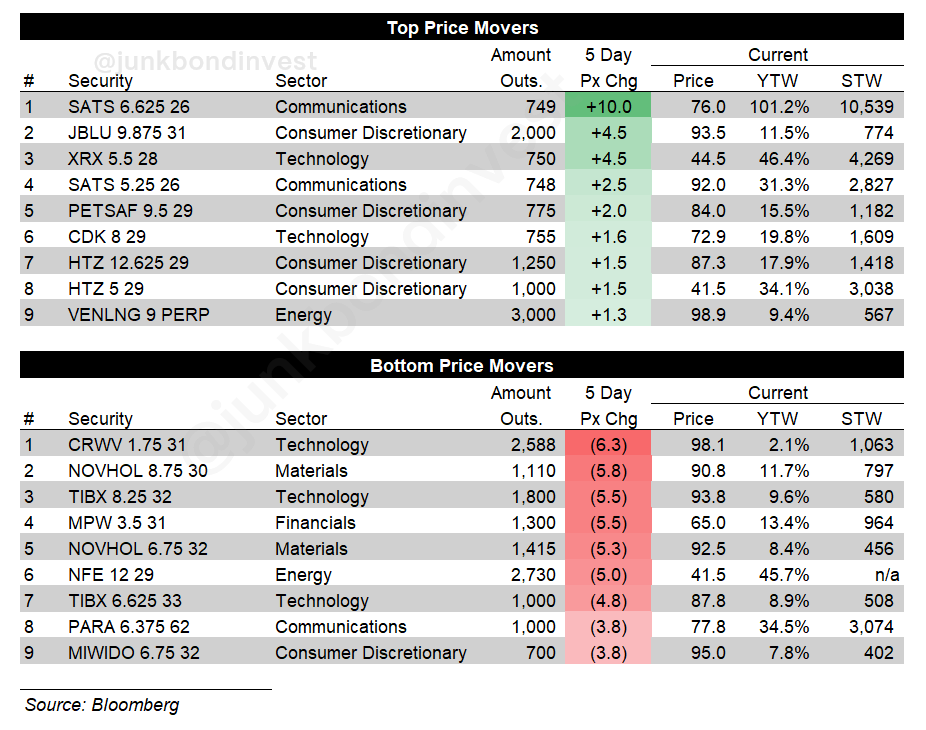

CCC spreads blowing through 700bps. HY funds posting their largest weekly outflow of the year. Recent new issues fading. Bids drifting to new lows while the primary market remained hot.

You missed it. Most people did. Which one you noticed says more about your positioning than about the market.

What $50 Billion in Orders Actually Means

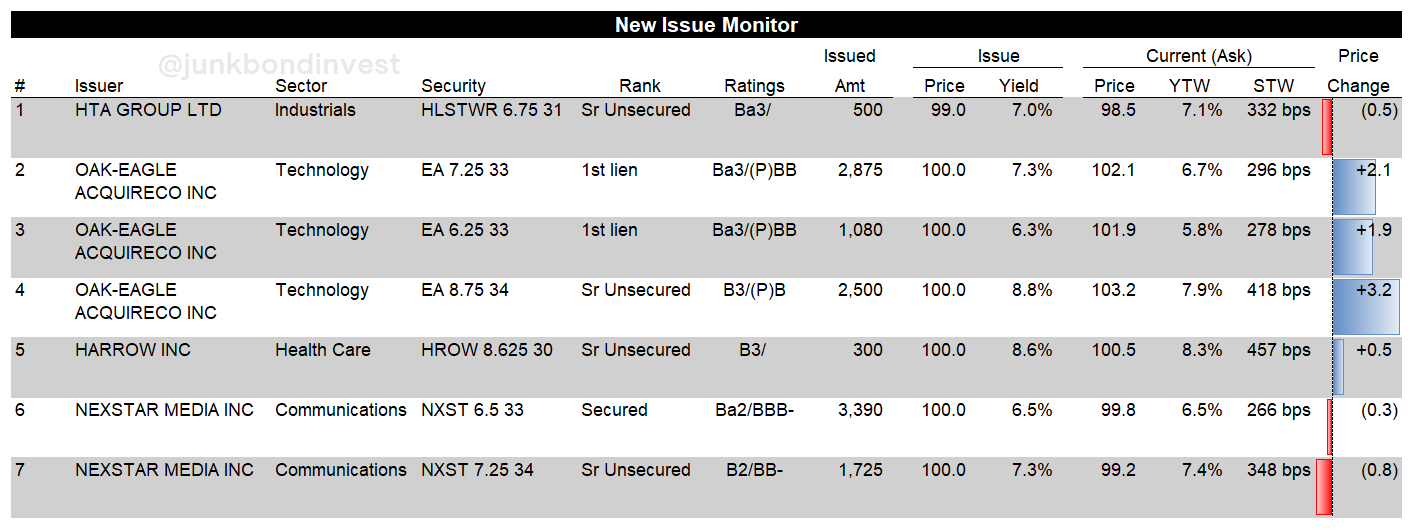

EA bulls felt vindicated. Fifty billion dollars. Five hundred accounts. The $2.875 billion of 7.25% secured notes hit 102 in the secondary. The $2.5 billion of 8.75% unsecureds up to 103. Investors were calling the pricing cheap for the rating.

The more skeptical read is that $50 billion in orders is not proof of health. It’s a sign of cash that has nowhere else to go and a market conditioned by fifteen years of buy-the-dip reflexes.

500 accounts chasing the same paper because rates are high enough to make the carry look attractive and everyone figures someone else stress-tested the macro assumptions underneath the deal. The biggest LBO financing since the GFC pricing tight in the same week that CCC spreads hit nine-month wides and HY funds posted their largest weekly outflow of the year.

Worth stepping back on what’s actually driving primary volume.

This is not a broad market reopening. EA, Nexstar, Sealed Air. M&A and LBO financings are carrying the entire market right now. Refi activity has collapsed. Strip out the acquisition financings and the primary market looks a lot quieter than the headline numbers suggest.

The appearance of health is concentrated in a handful of large transactions, not a broad return of risk appetite.

The Secondary Market Nobody Is Talking About

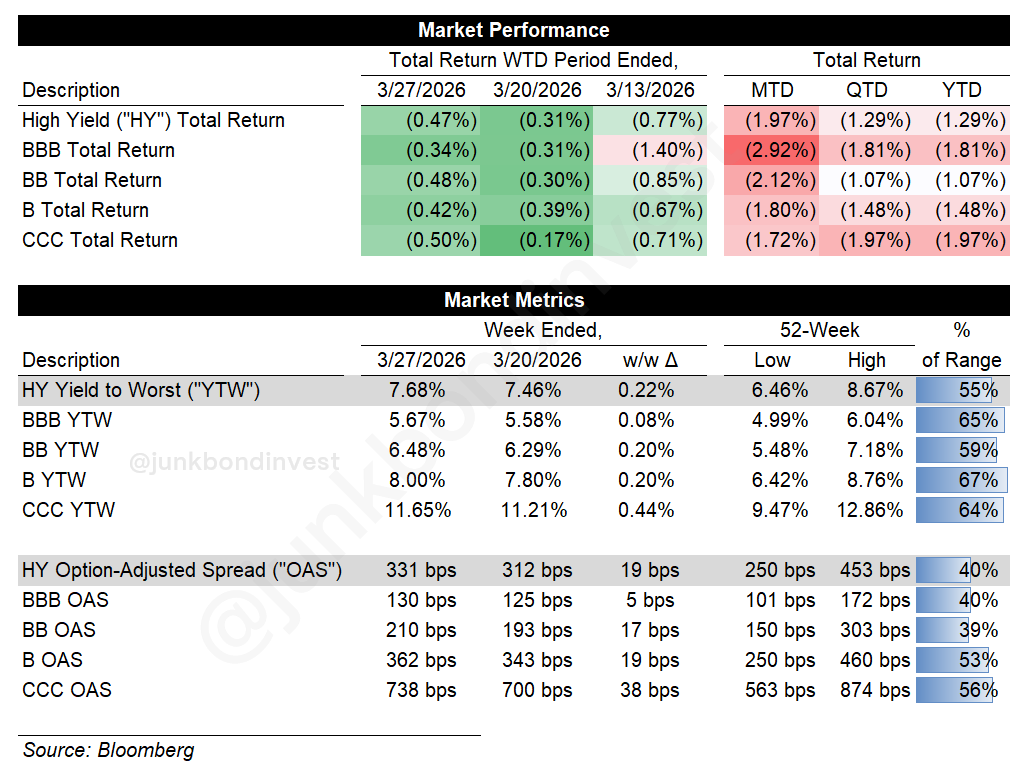

CCC spreads blew through 700bps last week, widest since June. BB yields climbed to a 10-month high. The Bloomberg US Corporate High Yield Total Return Index has returned -1.97% month to date. YTD returns are negative too. HY funds posted their largest weekly outflow of the year.

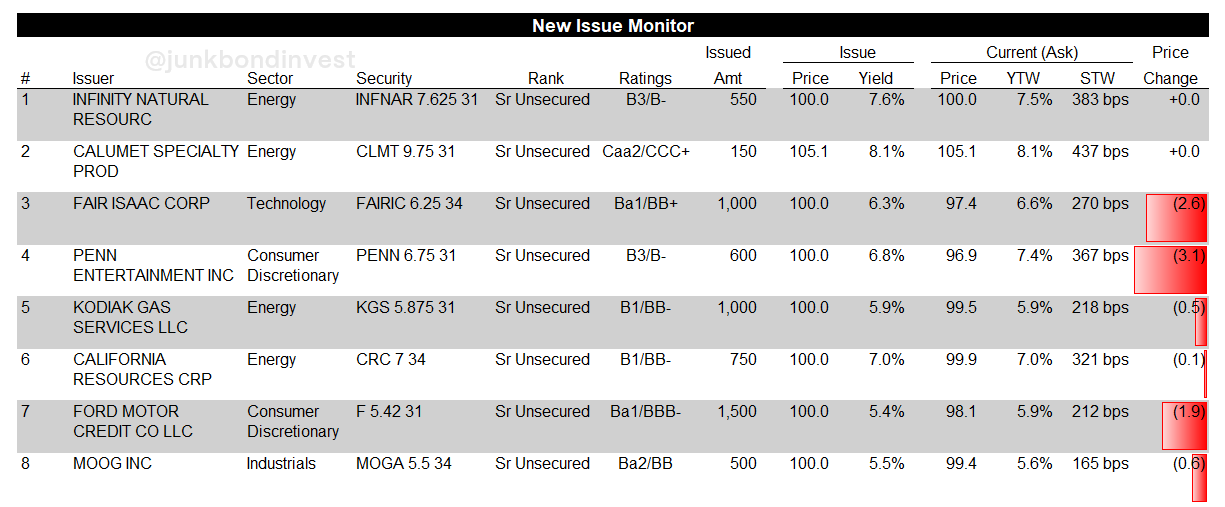

Recent deals are backsliding. FICO’s 6.25% notes at 97. PENN’s 6.75% bonds at new lows.

What’s also worth naming explicitly is what’s driving all of it.

Credit right now is behaving more as an output of oil and rates than anything happening at the issuer level. Spreads, yields, and risk appetite are being set by energy prices and Treasury moves first. Company-specific stories are layered on top. The macro is overriding the micro in a way that rarely persists but is very much the reality right now.

The credits that are actually moving are moving on events. Hertz jumped as travelers looked for alternatives to flying amid the TSA staffing crisis / hours-long airport security lines. JetBlue popped four points on M&A speculation.

Beneath the index level, the sector picture is increasingly divergent and it maps almost directly onto Iran exposure.

Energy is the one area of leveraged credit where fundamentals and geopolitics are pointing in the same direction. Improving credit profiles, genuinely under-owned, with a tailwind the market keeps treating as temporary. New deals pricing tight and trading up. One of the few places where primary and secondary are in agreement.

Everything with hydrocarbon input costs is moving the other way. Autos, building products, specialty chemicals, packaging. A 30% oil move doesn’t stay in the energy sector. It runs through every manufacturer with petroleum-based inputs and energy-intensive processes.

Building products and homebuilders had a weak earnings season with more issuers still to report. The sector was already dealing with soft housing and no policy support before Iran added an input cost layer on top. PE-backed structures built for a rate environment that never materialized are now facing a commodity shock on top. Price discovery in that sector is not done.

Consumer-facing credits are quietly getting harder to underwrite. Gas price expectations just hit their highest level since 2022. University of Michigan consumer sentiment slipped to a three-month low. Lower-income cohorts absorbing higher full-price costs while energy takes a bigger share of their wallet is a difficult backdrop for retailers, restaurants, and anything else levered to discretionary spending.

The sectors holding up are the ones with real assets, contracted cash flows, or a direct benefit from the energy price spike. Everything else is seeing a commodity shock, a rate shock, and a consumer confidence shock simultaneously. That combination was not in any of the underwriting models.

Why Iran Doesn’t Just Walk Back

The market keeps trying to trade this like a financial shock.

Financial shocks have circuit breakers. Rate cuts, liquidity injections, a policy reversal, the right statement at the right moment. You reverse the policy and the shock reverses with it. That’s why every tariff headline last year generated violent two-way price action. The underlying economy was intact. The damage was a decision, and decisions can be undecided.

Physical shocks don’t work that way. Infrastructure damage doesn’t reverse on a ceasefire. The supply disruption outlasts the conflict itself regardless of what the diplomatic calendar produces. That’s been true since the first week and it hasn’t changed.

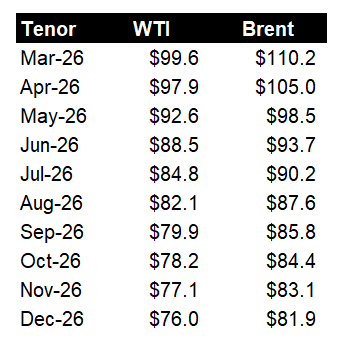

The oil futures curve has Brent in the $80s by August. Maybe that’s right.

But the Strait of Hormuz problem remains unsolved. Neither side has a clean exit. The escalation trap keeps ratcheting. The Houthis entering with risk to Bab al-Mandeb adds a second chokepoint and a third actor with its own incentive structure entirely.

Private Credit: The Ratchet Accelerates

The macro pressure is hitting an asset class that was already under strain before the conflict started.

Investors have sought to pull roughly $13 billion from over a dozen private credit funds so far this quarter. More than $4.6 billion is sitting behind withdrawal limits. Apollo, Ares, and BlackRock all capped at 5% after requests came in higher than that. All “normal course” as per the docs as they like to say.

Meanwhile, Cliffwater paid out 7% for the first time and now has a negative outlook from S&P. FS KKR got cut to junk by Moody’s (no surprise). Oaktree had to bring in Brookfield’s own balance sheet capital just to meet redemptions in full.

The structure was always the problem. Retail investors were sold quarterly liquidity against assets that take years to mature. Works fine until redemptions exceed inflows. All at the same time. And that’s BEFORE any major credit concerns.

At that point managers sell their best liquid assets first. The clean BSLs at or near par. The NAV stays roughly stable on paper because those sales happened at par. But the quality of the collateral behind the NAV quietly deteriorated with every redemption cycle.

The remaining portfolio becomes progressively more concentrated in the marks-at-model positions. The software loans, the PIK borrowers, the credits nobody wanted to buy. The fund looks fine until it doesn’t, and when it doesn’t the markdown is sudden because it’s been accumulating for quarters.

That selling also lands directly in the broadly syndicated secondary market as incremental supply at exactly the moment the secondary is already soft.

There’s a lot more to say here and a weekly recap isn’t the right format for it. Rather than jamming a nuanced private credit take, I’m launching a dedicated series on private credit starting later this week.

The redemption dynamics, the mark-to-model problem, the CLO feedback loop, the vintage exposure. All of it deserves its own treatment. Keep an eye out for that.