CoreCivic ($CXW): Beyond the Post-Election Rally

Analyzing the Multiple Paths to Value Creation After Trump's Win

🚨 Connect with me on Twitter / Instagram / Threads / Bluesky | Estimated Read Time: 18 Minutes

This week, I’ll be reviewing CoreCivic, Inc., one of two major publicly-traded private prison operators, whose shares have surged ~70% since Trump’s victory earlier this month. While I examined the sector back in July through my write-up on GEO Group (link), the shift in the political landscape warrants a fresh look at the sector, particularly given its strong operating momentum and improved balance sheet heading into this transition.

The stock’s recent performance raises important questions about both the magnitude and sustainability of potential benefits from a new Trump administration. With ICE populations already trending higher and border policy likely to take center stage in early 2025, I’ll attempt to frame the investment opportunity by examining realistic scenarios for detention populations, occupancy levels, and ultimate earnings power.

Let’s dive in and examine whether the bull case extends beyond the initial post-election enthusiasm. Separately, as a house keeping matter, I will be raising prices at year end. Anyone subscribing before then will be grandfathered into this year’s prices.

Situation Overview:

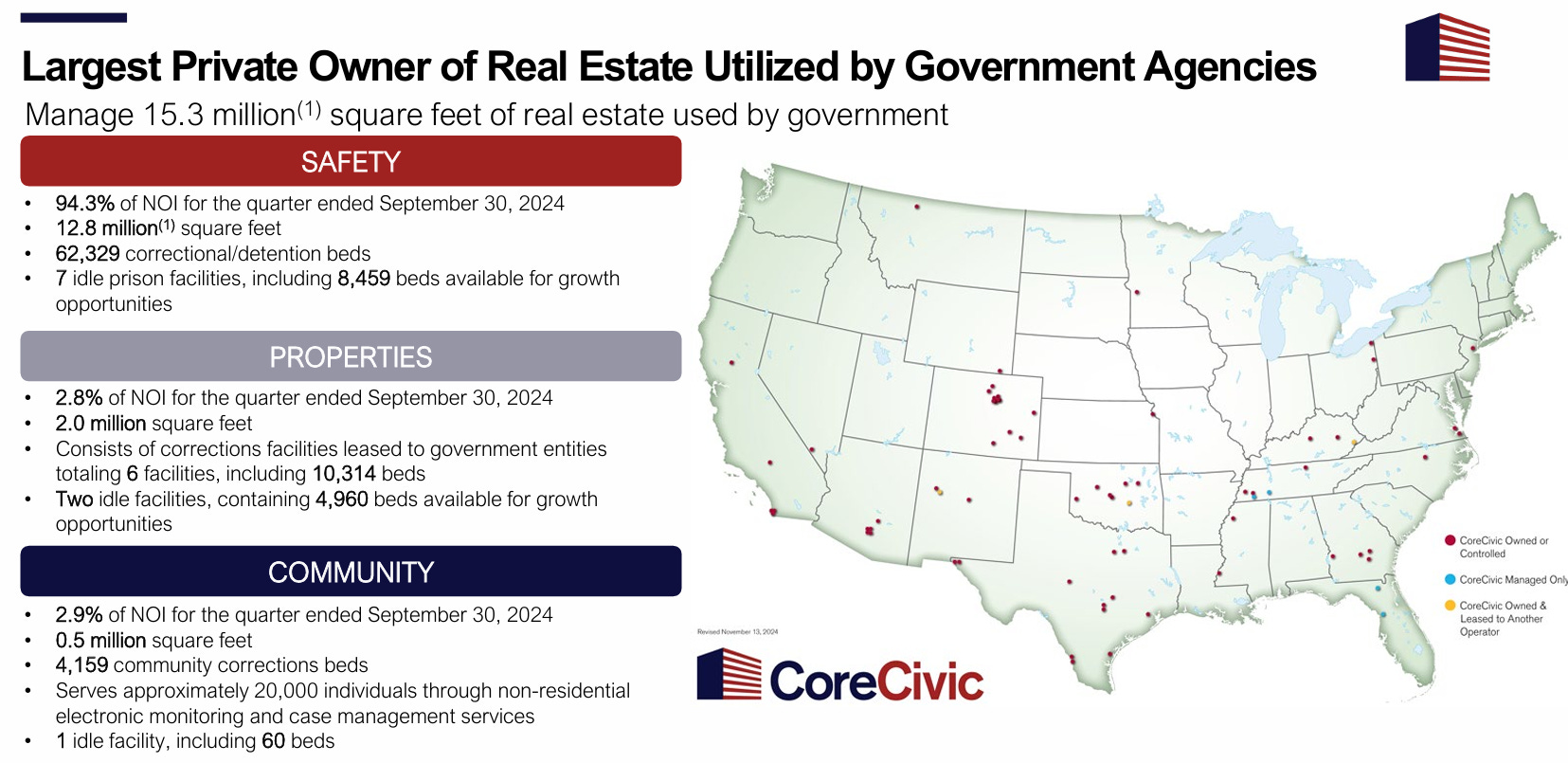

Founded in 1983 and headquartered in Brentwood, Tennessee, CoreCivic, Inc. (“CXW”) is one of the largest private operators of correctional and detention facilities in the United States. The company operates through three segments: CoreCivic Safety (91% of revenue), CoreCivic Community (6%), and CoreCivic Properties (3%). With a total bed capacity of ~76,000 across 69 facilities, CXW serves federal, state, and local government agencies through long-term contracts, maintaining a dominant market position in the private corrections industry.

Industry-Wide Challenges & Corporate Evolution

The private corrections industry faced significant headwinds beginning in 2019 when several major banks announced they would no longer provide financing to private prison operators, effectively “de-banking” the sector. The situation was further complicated by Biden’s 2021 executive order barring the renewal of contracts with privately operated criminal detention facilities by the Department of Justice. The COVID-19 pandemic added another layer of complexity, requiring rapid implementation of health protocols while dealing with reduced occupancy rates. In response to these challenges, CXW made the strategic decision to transition from a REIT to a C Corp in 2021, suspending dividend payments to redirect cash flow towards debt reduction and operational needs.