Cascades Inc. ($CAS): BB-Rated, But for How Long?

Bear Island still ramping, leverage still stuck, margins still capped.

🚨 Connect: Twitter | Threads | Instagram | Bluesky | Reddit

Something new is coming.

Built for people who actually care about credit. If you want a first look before it opens up, join the early access list (limited spots).

Everyone thinks they know Cascades. They don’t.

They see a BB-rating and think it’s safe. They see boxes and toilet paper and think it’s boring. They hear “Canadian paper company” and stop asking questions. But this credit? It’s not what it says it is.

You’re not buying a box maker. You’re buying a margin-constrained, fixed-cost machine that lives and dies by OCC prices and mill uptime. A business that spent half a billion dollars on a CapEx project that still isn’t running at plan. A name that’s been talking about deleveraging for four years and hasn’t moved an inch.

The tissue business is doing the heavy lifting while Bear Island drags and recycled fiber eats margins alive. Net leverage? Still over 4x. Interest cost? C$140 million and rising. There’s no covenant risk and no near-term maturity, but that doesn’t make this a good credit. It makes it a quiet one.

No, this is a credit that lives in the space between “it’s fine” and “why is it still like this?”

I. Situation Overview:

Cascades used to be the most boring business in the world…and that was the point. The Quebec-based paper and packaging company built a steady business around two simple ideas: turn recycled cardboard into new boxes, and make tissue paper for bathrooms and kitchens. Nothing sexy, but margins were predictable and cash flows were reliable.

Then management decided to make a big bet.

They spent US$525 million converting their Bear Island mill in Virginia to capitalize on the e-commerce boom and growing demand for containerboard. It was a bold capex call meant to expand margins. Instead, it’s been an 18-month drag on earnings, still running below target output, and emblematic of the broader issue: Cascades tried to get more efficient and wound up more fragile.

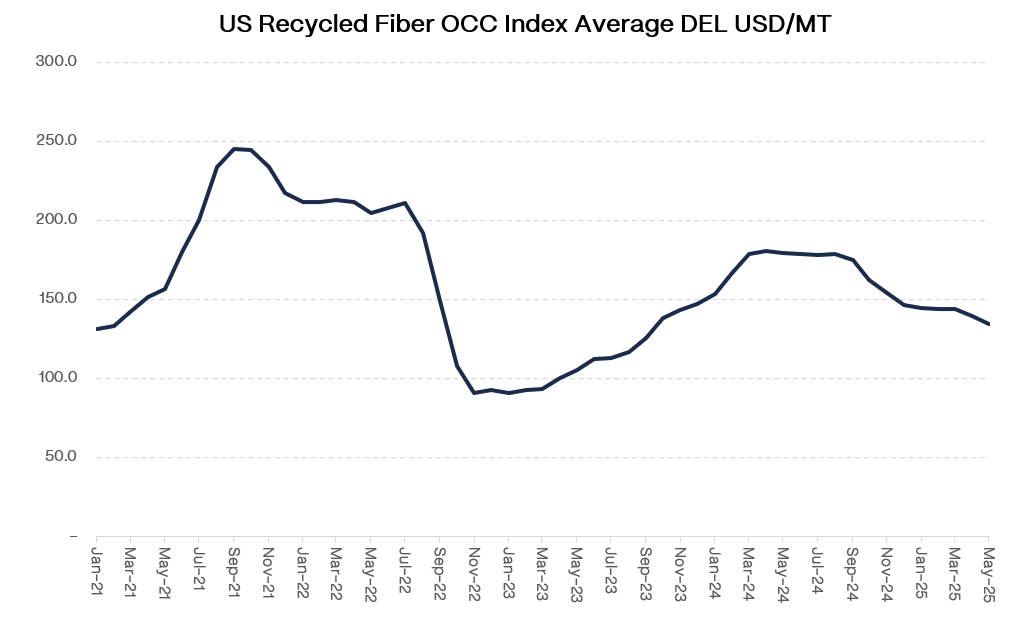

The bigger problem sits upstream however. Cascades sources the majority of its recycled fiber (OCC) from the open market, and the volatility has been crushing. Every $25/ton change in OCC swings EBITDA by ~C$61 million, and with no hedging or structural pass-through, margins have been on a roller coaster. OCC prices peaked at $245/ton in 2021, dropped to $90 in 2022, then climbed back to $190 in early 2024 before easing to $135/ton recently. The input curve alone explains half the EBITDA swings since 2021.