Blue Owl Technology Finance Corp ($OTF): Not as Cheap as It Looks

Why the 32% discount to NAV isn't the interesting number

Everyone loves a discount.

32% off reported NAV. A $17 stock trading at $11.82. Private credit, the hottest asset class of the last decade, suddenly democratized and available to anyone with a brokerage account.

You know the pitch. The market is wrong. Everyone is scared. You’re the smart money. You’re buying a dollar for 68 cents while the tourists panic.

But what if the market is not panicking? What if it has looked at this portfolio carefully and keeps arriving at the same conclusion?

OTF is a $14 billion portfolio of software loans, many tied to companies taken private at peak multiples during the free money era. Blue Owl manages it.

I went through the borrowers, reclassified the portfolio by what the companies actually do and when the deals were originated, then compared the marks against where similar paper is trading today.

The result was not comforting.

What OTF Actually Is

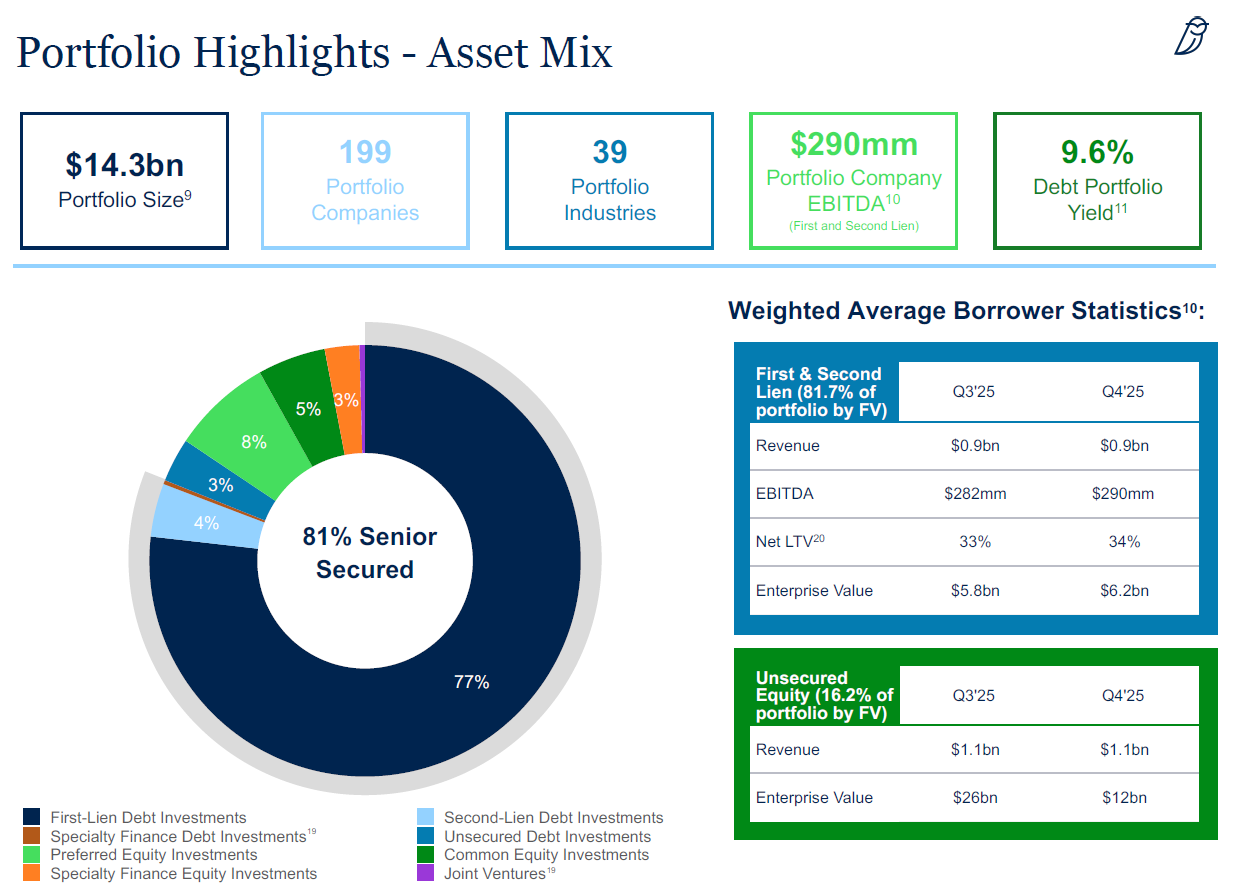

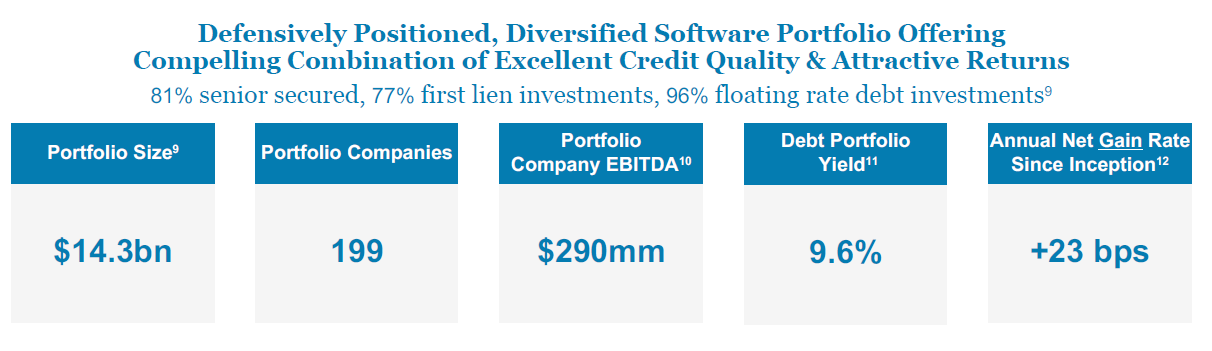

OTF is a $14.3 billion book of loans, almost entirely floating rate, to software and technology companies. Blue Owl manages it externally. The portfolio spans 199 companies across 39 industries, with 77% in 1L positions and avg. portfolio company EBITDA of $290 million. Leverage sits at 0.75x debt-to-equity, which is moderate by BDC standards.

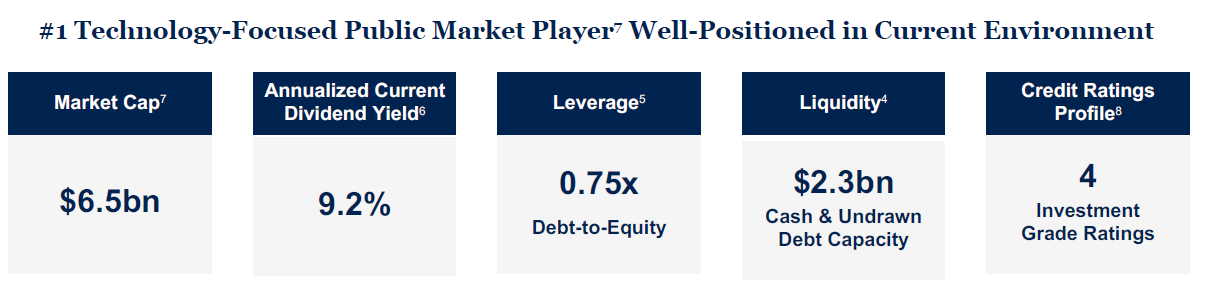

Liquidity, cash plus undrawn capacity, is $2.3 billion. At the current stock price of $11.82, the regular dividend alone yields 11.8% annualized, 13.5% including the special dividend. On paper, it looks like a well-structured vehicle offering attractive income from a diversified credit book.

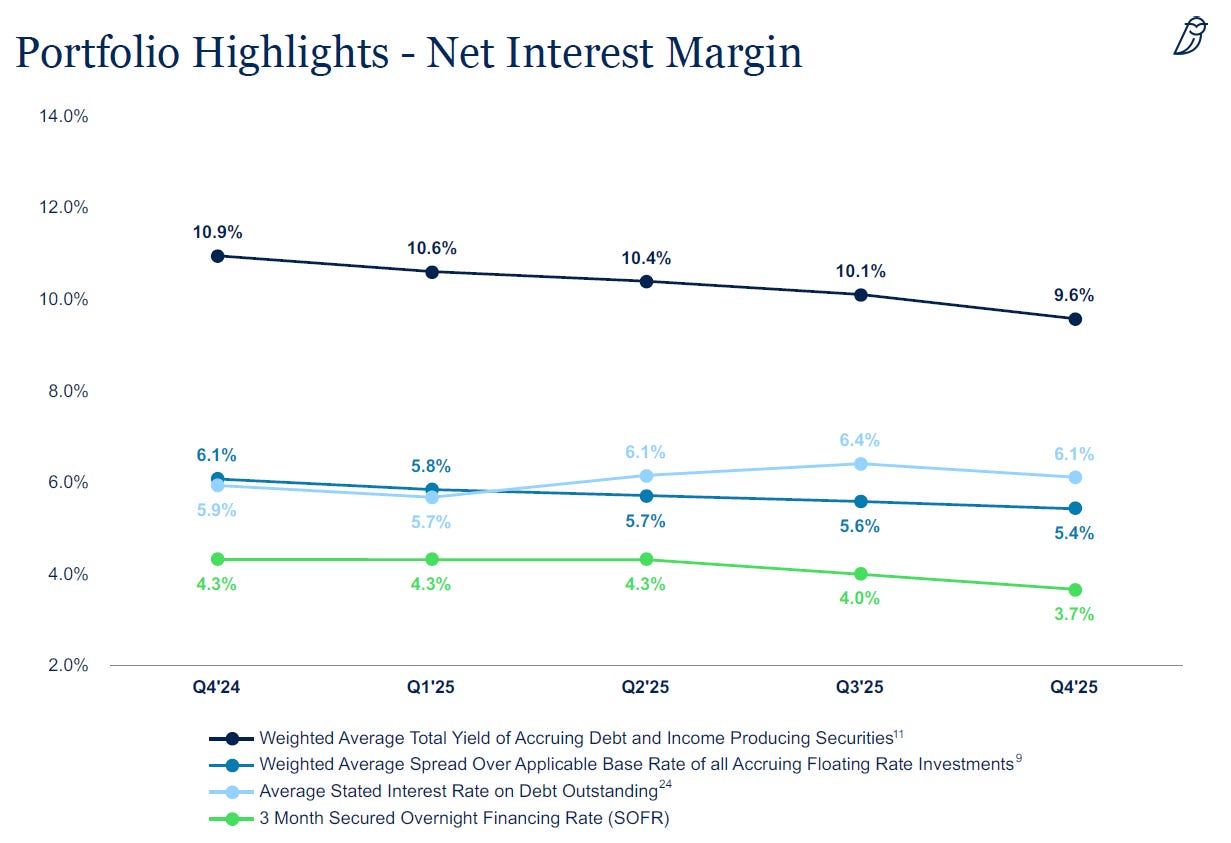

Two numbers from the filing are worth sitting with before accepting that framing. The first is the weighted average total yield on the portfolio, which fell from 10.9% in 4Q’24 to 9.6% by 4Q’25, a 130bps compression in a single year driven by SOFR moves.

The second is fair value as a percentage of principal on the debt book, which the filing reports at 99.2%. That number is not wrong. It is the number as of December 31, right before the tech sell-off. Both of those facts matter for what comes next.

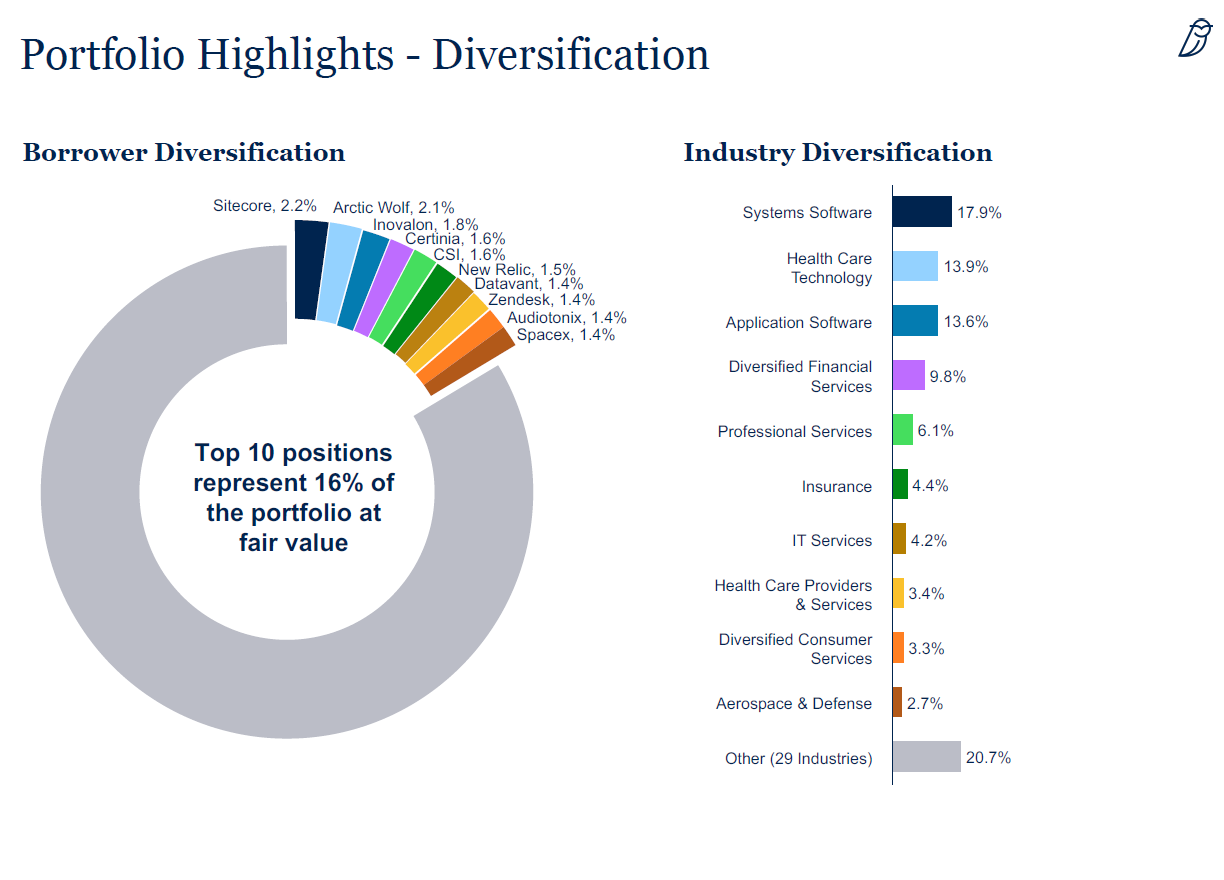

Blue Owl’s own investor deck describes OTF as a “Defensively Positioned, Diversified Software Portfolio.” That phrase is worth sitting with for a moment, because both adjectives are doing considerable work.

Start with “diversified.” OTF is explicitly a technology lender, so meaningful tech concentration is expected and by design. The issue is not the concentration itself. It is that the filed sector breakdown actively obscures its extent, with consequences for how investors model a tech credit event. The filing breaks exposure across buckets like Systems Software, Application Software, Health Care Technology, and Diversified Financial Services. Systems Software and Application Software combined come to 31.5%. That figure creates an impression of balance that the underlying portfolio does not support.

Now look at what they left out.