Air T, Inc ($AIRT): Aviation Oddball Meets 12% Trust Preferreds

Exploring Air T’s Unique Mix of Aviation Businesses and Strategic Potential

🚨 Connect with me on Twitter / Instagram / Threads / Bluesky | Estimated Read Time: 13 Minutes

Here’s a weird one for you: a holding company that flies planes for FedEx, trades jet engines, and sells de-icing trucks, all rolled into one messy $287 million revenue business. The stock bounces around between $10-40, currently sitting at $20, while management keeps “building for the long term” as they like to say. But what exactly are they building?

While most investors focus on the common stock, there’s another layer to this story: $34 million of trust preferred securities that almost nobody covers, trading at 68 cents on the dollar and yielding 12%. Understanding these TruPS—and their role in management’s strategy—requires untangling both the complex corporate structure and CEO Nick Swenson’s long-term vision.

The key question for both equity and credit investors is whether management can transform this collection of aviation assets into something greater than the sum of its parts. In a market obsessed with AI and meme coins, that might not sound exciting—but there’s something compelling about a company that actually moves things and fixes planes…

I. Situation Overview

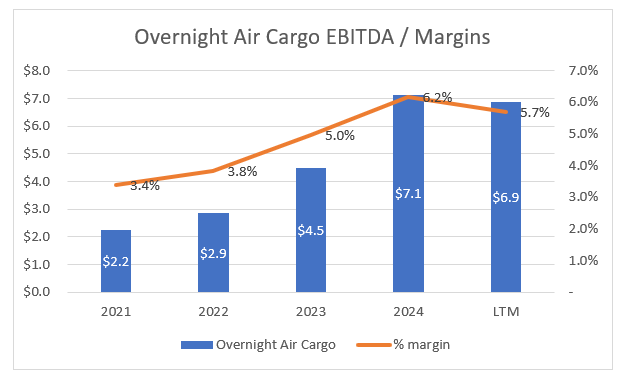

Let’s start with what Air T actually does—it’s a holding company operating 14 companies with 600+ employees. The foundation is their overnight cargo business, running 105 planes for FedEx’s feeder network. You know those smaller planes bringing packages to regional airports? That’s Air T.

They’ve been doing this since the early days, starting with flying dolphins for SeaWorld if you can believe it. FedEx represents 36% of revenue now, which sounds scary until you realize this relationship has lasted 40 years. The cargo partnership proved durable and expanding with Air T operating 66 aircraft for FedEx in 2021 to 105 planes today.

The cargo business generates steady ~6% margins but hasn’t shown huge improvement despite growing the fleet over the last year. Labor costs and infrastructure eat up the revenue gains. Still, it’s relatively stable cash flow as long as FedEx stays happy. And while FedEx can technically cancel with 10 days’ notice, good luck finding another operator who can run 105 planes across the eastern U.S. overnight network.